Cyberattacks cost businesses billions every year, yet many companies remain unprepared for the financial fallout of a major breach. Digital threats are growing more sophisticated, putting sensitive data and business operations at constant risk. Cyber insurance has become a vital shield for organizations facing these challenges, offering coverage that goes beyond basic security tools. This guide breaks down what cyber insurance covers, who needs it, and how it can protect your business from digital dangers.

Cyber Insurance Guide: Comprehensive Table of Contents

- What Is Cyber Insurance Coverage?

- Types of Cyber Insurance Policies

- Key Features and Exclusions Explained

- Claims Process and Response Expectations

- Cost Factors and Risk Assessment

- Common Mistakes and How to Avoid Them

Key Takeaways

| Point | Details |

|---|---|

| Importance of Cyber Insurance | Cyber insurance serves as a financial safety net, protecting businesses from digital threats and covering expenses related to data breaches and legal liabilities. |

| Types of Coverage | Cyber insurance policies generally include first-party and third-party coverage, addressing internal losses and external liabilities, respectively. |

| Claims Process | Effective navigation of the claims process involves immediate reporting, thorough documentation, and working closely with insurers to ensure coverage eligibility. |

| Pricing Factors | Key determinants of cyber insurance costs include company size, industry risk, data sensitivity, and existing cybersecurity measures, necessitating careful risk assessment and management. |

What Is Cyber Insurance Coverage?

Cyber insurance is a specialized risk management tool designed to protect businesses from financial losses resulting from digital threats and cyber incidents. According to the FTC, cyber insurance helps businesses mitigate losses by covering expenses related to data breaches, network damage, and potential legal liabilities.

Typically, cyber insurance policies provide comprehensive financial protection against a range of digital risks. As the GAO explains, these policies cover critical costs such as:

- Data recovery expenses

- Legal fees associated with cyber incidents

- Business interruption losses

- Forensic investigation costs

- Potential regulatory compliance penalties

Think of cyber insurance like a digital safety net for your organization. Just as traditional business insurance protects against physical risks, cyber insurance safeguards your digital assets and financial stability. It’s not just about covering immediate damages but also providing resources for comprehensive incident response and recovery.

Businesses across various sectors – from healthcare and finance to retail and technology – are increasingly recognizing cyber insurance as a crucial component of their risk management strategy. Understanding cyber insurance basics can help you determine the right level of protection for your unique operational needs.

Types of Cyber Insurance Policies

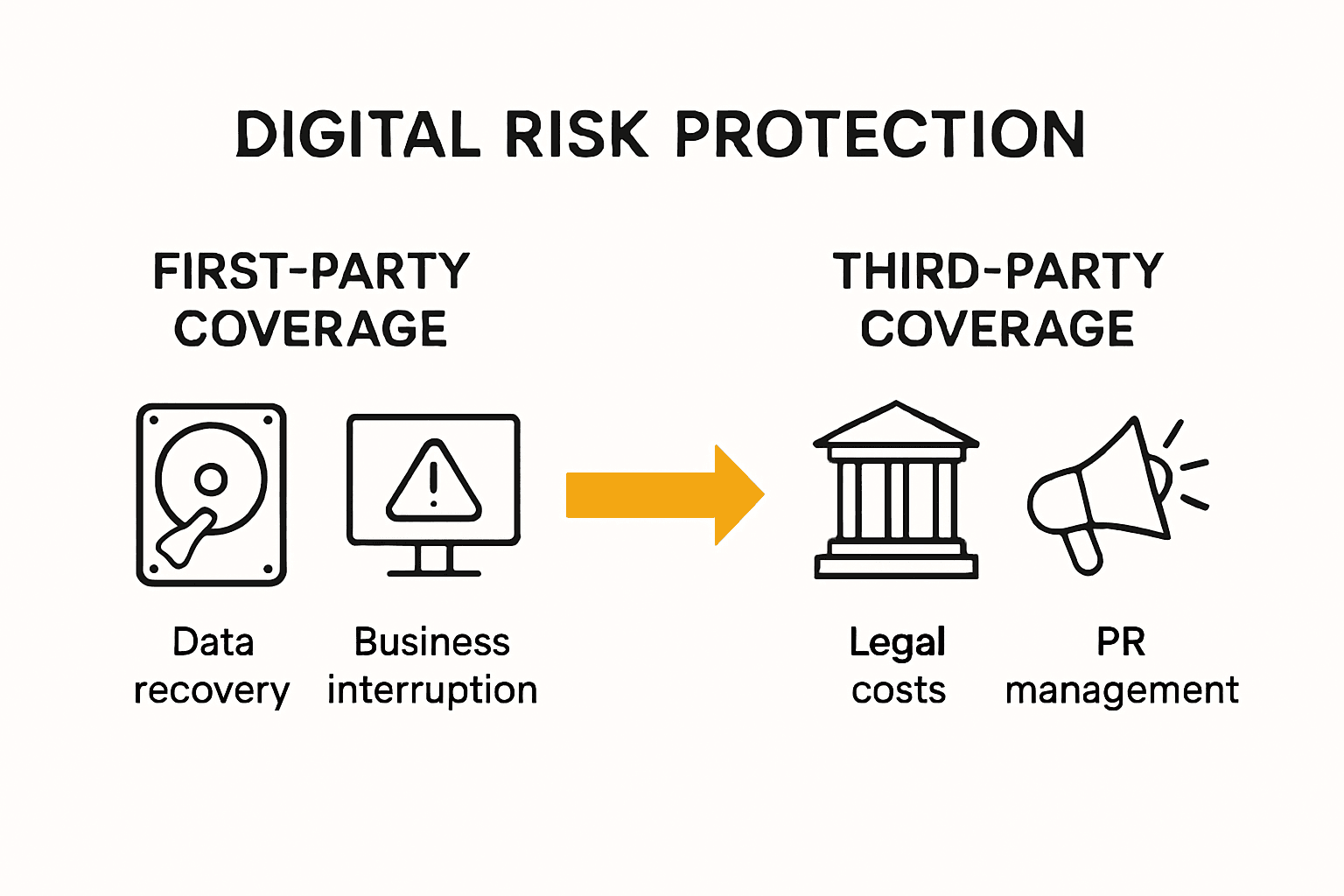

Cyber insurance policies are not one-size-fits-all solutions. According to the FTC, these policies typically include two primary coverage categories: first-party coverage and third-party coverage. Understanding the nuances of each type is crucial for comprehensive digital risk management.

First-Party Coverage addresses direct losses experienced by an organization. As Cambridge Health explains, this coverage handles expenses an organization incurs directly from a cyber incident, including:

- Data recovery costs

- Business interruption expenses

- Cyber extortion payments

- Notification and credit monitoring for affected customers

- Forensic investigation expenses

Third-Party Coverage focuses on external liabilities arising from cyber incidents. This protection helps businesses manage legal and financial risks associated with data breaches that impact clients, customers, or partners. Typical third-party coverage includes:

- Legal defense costs

- Settlement expenses

- Regulatory compliance penalties

- Customer lawsuit settlements

- Public relations and reputation management expenses

While choosing a cyber insurance policy, businesses should carefully evaluate their unique risk profile and select coverage that aligns with their specific operational vulnerabilities. Understanding cyber insurance overview can provide deeper insights into crafting a robust digital risk management strategy.

Key Features and Exclusions Explained

Cyber insurance is a complex protective tool with specific inclusions and limitations. According to the FTC, policies typically include key features such as coverage for data breaches, network security failures, and cyber extortion. However, understanding these features requires a nuanced approach to risk management.

Key Coverage Features

Most comprehensive cyber insurance policies provide protection for:

- Digital asset restoration

- Incident response costs

- Legal and regulatory expenses

- Business interruption losses

- Ransomware payment support

- Forensic investigation expenses

Critical Exclusions

As Security.org highlights, cyber insurance policies often exclude critical areas such as:

- General liability claims

- Property damage

- Employment practices liability

- Intellectual property theft

- Intentional acts by the insured organization

Businesses must carefully review policy details to understand exactly what is and isn’t covered. Some policies may exclude scenarios like acts of war, state-sponsored cyber attacks, or losses resulting from known vulnerabilities that weren’t patched.

Understanding cyber insurance overview can help organizations navigate these complex coverage landscapes and make informed decisions about their digital risk protection strategy.

Claims Process and Response Expectations

Navigating a cyber insurance claim requires strategic preparation and immediate action. According to the FTC, policyholders should promptly notify their insurer when a cyber incident occurs, typically through a dedicated breach hotline. Quick and comprehensive communication is critical to initiating the claims process effectively.

Key Steps in the Claims Process

The cyber insurance claims process typically involves several crucial stages:

- Immediate Incident Reporting

- Contact your insurance provider immediately

- Provide comprehensive initial incident details

- Request guidance on immediate response actions

- Documentation and Evidence Gathering

- Collect all relevant system logs

- Preserve digital forensic evidence

- Document financial and operational impacts

- Insurer Assessment and Response

- Insurer coordinates with forensic experts

- Evaluate claim’s eligibility and coverage

- Determine potential reimbursement strategy

As the Cyber Readiness Institute explains, the claims process involves thorough assessment and coordination between the policyholder and response teams. The insurer will work to cover eligible costs as outlined in the specific policy terms.

Understanding cyber insurance overview can provide additional insights into effectively managing cyber insurance claims and preparing your organization for potential digital security incidents.

Cost Factors and Risk Assessment

Cyber insurance pricing is a complex calculation that goes beyond simple risk evaluation. According to the Government Accountability Office (GAO), insurers face significant challenges in pricing policies due to limited historical data, which often results in higher premiums and more stringent policy terms for businesses.

Key Pricing Determinants

Multiple factors influence the cost of cyber insurance coverage:

- Company Size: Larger organizations typically face higher premiums

- Industry Sector: High-risk industries like healthcare and finance pay more

- Data Sensitivity: Organizations handling critical personal or financial data incur higher costs

- Current Cybersecurity Infrastructure: Robust security measures can reduce premiums

As Tech UK explains, the cost is directly tied to an organization’s existing cybersecurity posture. Businesses with comprehensive security protocols, regular risk assessments, and proactive threat management strategies are viewed more favorably by insurers.

Risk assessment involves a detailed evaluation of an organization’s digital vulnerabilities. Insurers will typically conduct thorough assessments examining:

- Network security configurations

- Employee cybersecurity training

- Incident response capabilities

- Historical breach experiences

- Compliance with industry security standards

Understanding cyber insurance overview can provide additional insights into navigating the complex landscape of cyber insurance pricing and risk assessment.

Common Mistakes and How to Avoid Them

Navigation of cyber insurance requires careful attention to detail and strategic planning. According to the Construction Financial Management Association (CFMA), businesses frequently make critical errors that can compromise their digital risk protection strategy.

Top Cyber Insurance Pitfalls

Businesses commonly stumble into several key mistakes:

- Underestimating Cyber Risks

- Assuming “it won’t happen to me”

- Failing to conduct comprehensive risk assessments

- Overlooking potential vulnerability points

- Inadequate Policy Understanding

- Skipping detailed policy exclusions review

- Assuming broad coverage

- Not asking specific questions about limitations

- Misaligned Coverage

- Selecting generic policies

- Neglecting industry-specific risks

- Not customizing protection to organizational needs

As Tech UK emphasizes, one of the most significant errors is assuming existing insurance policies provide comprehensive cyber protection. Businesses must obtain standalone cyber policies to ensure genuine digital risk management.

To mitigate these risks, organizations should:

- Conduct thorough internal cybersecurity assessments

- Work closely with specialized insurance consultants

- Regularly review and update coverage

- Invest in ongoing cybersecurity training

Understanding cyber insurance overview can provide additional strategic insights for navigating these complex protection landscapes.

Strengthen Your Cybersecurity with Expert IT Support from SRS Networks

The article highlights how critical cyber insurance is for protecting your business from cyber risks like data breaches, ransomware, and legal liabilities. However, even the best cyber insurance cannot replace strong cybersecurity measures that reduce risks and make your insurance coverage more effective and affordable. If you are concerned about understanding your organization’s cyber risk profile and ensuring you have the right digital protections in place, SRS Networks is your trusted partner for tailored IT solutions.

Protecting your business starts with proactive cybersecurity services like endpoint protection, network security, and incident response planning, all combined with expert guidance on compliance and risk assessments. At SRS Networks, we specialize in crafting customized IT roadmaps that align with your unique risks and industry challenges. Don’t wait until a costly cyber incident happens—strengthen your defenses now and support your cyber insurance strategy with reliable IT management. Learn more about our comprehensive Cybersecurity Solutions and see how we help local businesses in Monterey Bay stay secure and grow confidently.

Frequently Asked Questions

What is cyber insurance coverage?

Cyber insurance is a risk management tool designed to protect businesses from financial losses due to digital threats and incidents, covering expenses related to data breaches, network damage, and legal liabilities.

What types of cyber insurance policies are available?

Cyber insurance policies typically include two primary coverage categories: first-party coverage, which addresses direct losses to an organization, and third-party coverage, which focuses on external liabilities arising from cyber incidents.

What are the key features and exclusions of cyber insurance?

Key features of cyber insurance include protection for data breaches, network security failures, and cyber extortion. Exclusions often involve general liability claims, property damage, and intentional acts by the insured organization.

How is the cost of cyber insurance determined?

The cost of cyber insurance is influenced by factors such as company size, industry sector, data sensitivity, and current cybersecurity infrastructure. Insurers assess an organization’s digital vulnerabilities to determine premiums.

Recommended

- Understanding Cyber Insurance Overview for Businesses – SRS Networks

- Understanding Cyber Insurance: A Comprehensive Guide – SRS Networks

- Cyber Insurance Basics: Everything You Need to Know – SRS Networks

- Understanding Cybersecurity for Small Business – SRS Networks

- How you can protect yourself from being hacked-Cyber Security Guide