Cyber attacks cost businesses billions every year, with one data breach averaging over $4 million in damages. The risk is not just for large corporations—small and midsize companies now face the same digital threats that can bring operations to a halt. As cyber risks grow, cyber insurance offers a vital layer of protection, helping organizations manage financial fallout, recover faster, and safeguard their reputation in a world where even a single hack can spell disaster.

Cyber Insurance Guide: Coverage, Eligibility and Claims Roadmap

- Defining Cyber Insurance And Its Importance

- Key Types Of Cyber Insurance Coverage

- What Cyber Insurance Policies Typically Include

- Understanding Eligibility And Policy Requirements

- Navigating Claims, Exclusions, And Costs

Key Takeaways

| Point | Details |

|---|---|

| Importance of Cyber Insurance | Cyber insurance is essential for businesses to mitigate financial losses from cyber attacks, covering costs like data breaches and business interruptions. |

| Types of Coverage | Understanding first-party and third-party coverage is vital for organizations to adequately protect their digital assets and meet various liability needs. |

| Policy Exclusions | Businesses must carefully review policy exclusions, such as infrastructure failures and state-sponsored attacks, to ensure comprehensive protection. |

| Preparation for Eligibility | Organizations should enhance their cybersecurity measures and develop incident response plans prior to applying for cyber insurance to improve eligibility prospects. |

Defining Cyber Insurance and Its Importance

In today’s digital world, businesses face an increasingly complex landscape of cybersecurity threats that can devastate operations overnight. Cyber insurance has emerged as a critical financial protection strategy for organizations seeking to mitigate potential digital risks. According to the Federal Trade Commission, cyber insurance helps protect businesses against substantial financial losses resulting from cyber attacks, covering crucial expenses like data breaches, business interruption, and legal fees.

At its core, cyber insurance operates as a specialized risk management tool designed to help organizations recover from digital disasters. The Indiana State Government explains that these policies specifically cover financial risks stemming from unauthorized network access and potential disclosure of confidential information. This means when a cybersecurity incident occurs, businesses aren’t left bearing the entire financial burden alone.

Key components of comprehensive cyber insurance typically include:

- Data Breach Response Costs: Covering expenses related to investigating and managing a security incident

- Legal Expenses: Supporting potential litigation and regulatory compliance challenges

- Business Interruption Coverage: Compensating for lost revenue during system downtime

- Reputation Management: Helping organizations rebuild trust after a significant cyber event

For small to medium-sized businesses in sectors like healthcare, manufacturing, and professional services, cyber insurance isn’t just a luxury – it’s becoming an essential strategic investment. The potential financial impact of a significant cyber incident can far outweigh the relatively modest premiums, making these policies a smart risk management approach in our increasingly interconnected digital ecosystem.

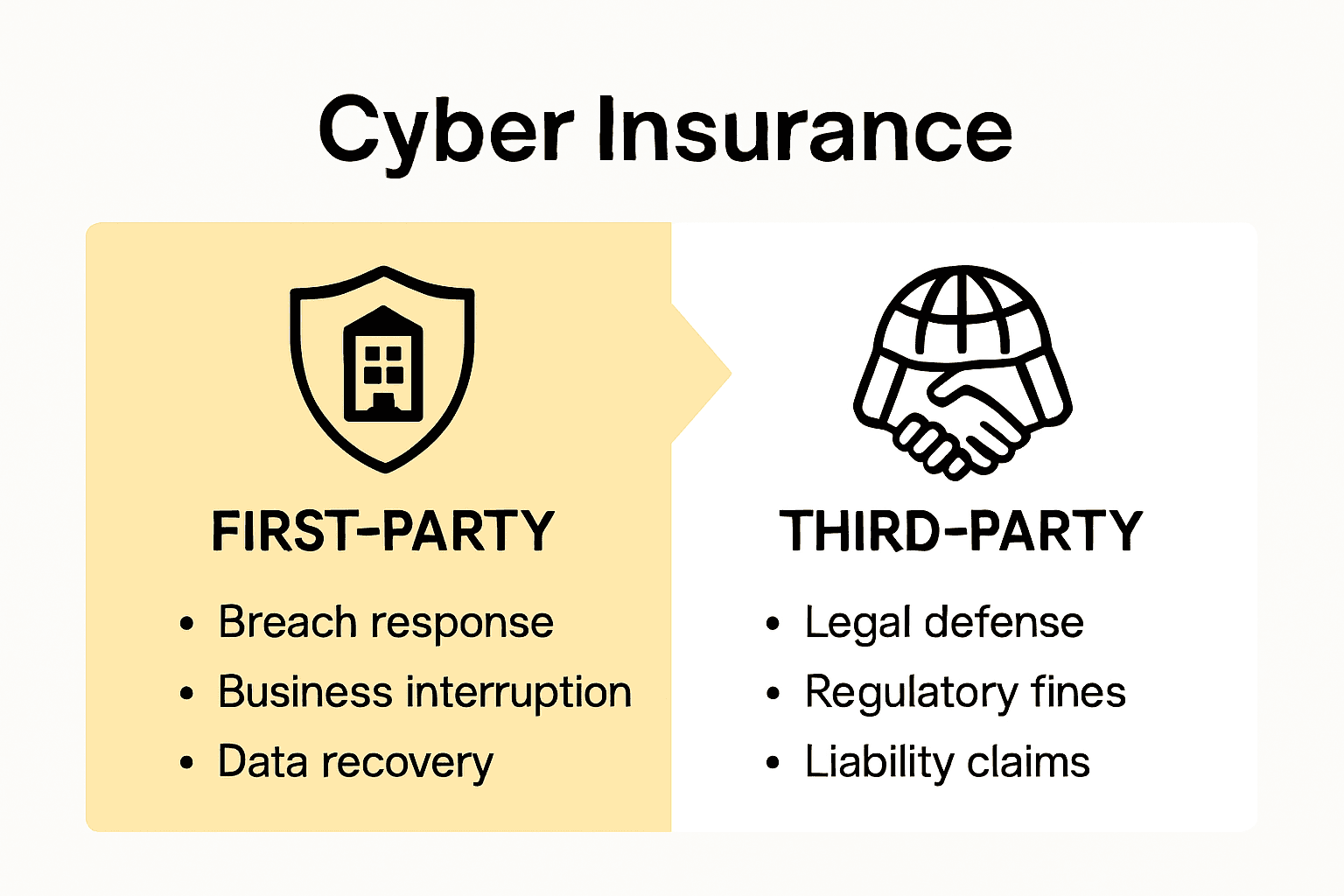

Key Types of Cyber Insurance Coverage

Navigating the complex world of cyber insurance requires understanding the different types of coverage available to businesses. First-party coverage and third-party coverage represent the two primary categories that organizations need to consider when protecting their digital assets. According to the Permanent Risk Management Program, cyber liability programs offer comprehensive protection spanning multiple critical areas of digital risk.

First-party coverage focuses directly on protecting the insured organization’s own losses. Lewis-Clark State College explains that this type of coverage addresses immediate financial impacts experienced by the business itself. Key components typically include:

- Data Breach Expenses: Costs associated with investigating and responding to a security incident

- Business Interruption Loss: Compensation for revenue lost during system downtime

- Cyber Extortion: Financial protection against ransomware and digital blackmail attempts

- Data Recovery Costs: Expenses related to restoring or reconstructing compromised digital information

Third-party coverage, by contrast, protects businesses against potential liabilities to external parties. This coverage becomes crucial when an organization’s cyber incident impacts clients, partners, or other stakeholders. Comprehensive third-party coverage often includes:

- Legal Defense Costs: Supporting potential litigation arising from data breaches

- Regulatory Penalties: Covering fines and expenses related to compliance violations

- Privacy Notification Expenses: Managing communication and support for affected individuals

- Reputation Management: Helping mitigate potential brand damage from cyber incidents

For small to medium-sized businesses across industries like healthcare, technology, and professional services, understanding these nuanced coverage types is essential. The right cyber insurance strategy isn’t about purchasing the most expensive policy, but selecting a comprehensive approach that matches your specific digital risk profile and organizational vulnerabilities.

Here’s a side-by-side comparison of first-party and third-party cyber insurance coverage:

| Coverage Component | First-Party Coverage | Third-Party Coverage |

|---|---|---|

| Primary Focus | Protects the insured’s own losses | Protects against external liabilities |

| Examples | Data breach response Business interruption Cyber extortion Data recovery |

Legal defense Regulatory penalties Privacy notifications Reputation management |

| Triggers | Direct attack or data loss | Claims from clients or regulators |

| Beneficiaries | The insured organization | Clients, partners, affected individuals |

What Cyber Insurance Policies Typically Include

Understanding the comprehensive scope of cyber insurance policies is crucial for businesses seeking robust digital protection. According to the Federal Trade Commission, these policies typically cover a wide range of potential digital threats, including data breaches, cyber attacks on vendor-held data, business interruption, crisis management, and cyber extortion.

The landscape of cyber insurance coverage can be complex, but most policies are strategically designed to address both immediate and long-term digital risks. The Reinsurance Association of America highlights that policies generally encompass two primary coverage categories:

First-Party Coverage Components:

- Direct Incident Response: Costs associated with investigating and managing a cyber incident

- Business Interruption Losses: Financial compensation for revenue disruptions

- Data Restoration: Expenses related to recovering or reconstructing compromised digital assets

- Cyber Extortion: Protection against ransomware and digital blackmail attempts

Third-Party Coverage Components:

- Legal Defense: Support for potential litigation resulting from cyber incidents

- Regulatory Compliance: Coverage for penalties and fines related to data protection violations

- Client Notification: Expenses for communicating with affected stakeholders

- Reputation Management: Strategies and resources to mitigate brand damage

For small to medium-sized businesses across various sectors, these comprehensive policies represent more than just financial protection – they’re a critical strategic investment in digital resilience. The right cyber insurance policy acts as a safety net, providing organizations with the resources and support needed to navigate the increasingly complex landscape of digital risks and potential cyber threats.

Understanding Eligibility and Policy Requirements

Securing cyber insurance isn’t a one-size-fits-all process. Different providers have unique criteria for determining which organizations qualify for coverage, making it essential for businesses to understand the specific requirements. According to PRISM Risk Management, obtaining cyber liability coverage typically involves completing a comprehensive cyber application, participating in specific coverage programs, and receiving approval from both carrier and oversight committees.

The eligibility process typically involves a detailed assessment of an organization’s existing cybersecurity infrastructure and risk management practices. Insurers want to see that businesses have implemented robust security measures that minimize potential vulnerabilities. Key elements they evaluate include:

- Current Cybersecurity Protocols: Existing network protection strategies

- Data Management Practices: How sensitive information is stored and protected

- Incident Response Plans: Documented procedures for handling potential cyber threats

- Technology Infrastructure: Current systems and their inherent security capabilities

Some providers, like the Local Government Insurance Trust, offer innovative approaches to cyber coverage. They provide protection for critical risks such as hacking, data breaches, and theft of personally identifiable information, often including legal mandates for victim notification. This approach demonstrates the evolving nature of cyber insurance, which goes beyond simple financial protection to include comprehensive risk management support.

For small to medium-sized businesses, the key is preparation. Before applying for cyber insurance, organizations should conduct thorough internal assessments, strengthen their cybersecurity posture, and develop clear, comprehensive incident response strategies. The more proactively a business can demonstrate its commitment to digital security, the more attractive it becomes to potential insurers. Remember, cyber insurance isn’t just about obtaining a policy – it’s about creating a robust framework of digital risk management that protects your organization’s most valuable assets.

Navigating Claims, Exclusions, and Costs

Cyber insurance represents a critical financial safety net, but understanding its nuanced landscape requires careful examination of claims processes, policy exclusions, and associated costs. According to the Reinsurance Association of America, cyber insurance policies often come with specific exclusions that businesses must carefully evaluate. These typically include scenarios such as infrastructure failures, nation-state attacks, voluntary system shutdowns, and certain types of system failures.

Key Policy Exclusions to Understand:

- Infrastructure Vulnerabilities: Losses stemming from known systemic weaknesses

- State-Sponsored Attacks: Cyber incidents attributed to government-level interventions

- Intentional Disruptions: Losses resulting from deliberate organizational actions

- Intellectual Property Consequences: Long-term impacts beyond immediate financial damages

The financial structure of cyber insurance can be complex. The Permanent Risk Management Program provides insights into typical coverage limits, demonstrating that policies can offer substantial protection. For instance, some programs provide up to $20 million in coverage per member, with a broader $120 million program aggregate. Most policies also incorporate a retention mechanism, often around $50,000, with options for organizations to adjust their risk exposure through buy-down retention strategies.

For small to medium-sized businesses, navigating these intricate details requires a strategic approach. Carefully review policy language, understand specific exclusions, and work closely with insurance providers to craft a comprehensive cyber insurance strategy. The goal isn’t just financial protection, but creating a robust risk management framework that adapts to your organization’s unique digital landscape. Remember, the most effective cyber insurance isn’t about finding the cheapest policy, but selecting comprehensive coverage that truly understands and mitigates your specific technological vulnerabilities.

Protect Your Business with Expert Cybersecurity and Support from SRS Networks

The article highlights the growing risks businesses face from cyber threats and how cyber insurance plays a vital role in mitigating financial losses from incidents like data breaches and ransomware attacks. If you are concerned about the complex eligibility requirements, policy exclusions, and the costly aftermath of cyber incidents it is essential to build a strong digital defense first. Without a solid cybersecurity strategy and real-time protection, even the best cyber insurance policy may not fully safeguard your business.

At SRS Networks, we specialize in helping small to medium-sized businesses across the Monterey Bay Area defend against cyber risks before they lead to costly claims. Our customized Cybersecurity Solutions include endpoint protection, firewalls, email security, and compliance support designed to reduce vulnerabilities and meet insurance eligibility criteria. Combine this with our Managed IT Services and Data Backup & Business Continuity offerings and you gain a trusted partner to secure your network, quickly respond to threats, and keep your operations resilient.

Ready to move beyond simply understanding cyber insurance to actually reducing your risk and protecting your business assets with proactive IT strategies?

Contact SRS Networks today and take the essential next step to safeguard your company. Visit https://srsnetworks.net to learn how our personalized, local IT services help you meet compliance needs, prevent digital disasters, and create peace of mind. Don’t wait until an incident happens. Let us help you build a stronger defense now.

Frequently Asked Questions

What is cyber insurance?

Cyber insurance is a specialized financial protection strategy designed to help businesses mitigate potential financial losses resulting from cyber attacks, data breaches, business interruptions, and legal fees associated with cybersecurity incidents.

What types of coverage are available in cyber insurance policies?

Cyber insurance policies typically offer two main types of coverage: first-party coverage, which protects the insured’s own losses, such as data breach expenses and business interruption, and third-party coverage, which covers liabilities to external parties, including legal defense costs and regulatory penalties.

What does a typical cyber insurance policy include?

A typical cyber insurance policy includes various components such as direct incident response costs, business interruption coverage, data recovery expenses, legal defense support, and reputation management strategies to mitigate the impacts of a cyber incident.

How can a business prepare for obtaining cyber insurance?

To prepare for obtaining cyber insurance, businesses should conduct thorough internal assessments, strengthen their cybersecurity protocols, develop incident response plans, and demonstrate their commitment to minimizing vulnerabilities in order to attract potential insurers.