Digital threats are hitting businesses harder than ever and cyber insurance has quickly moved from a nice-to-have to a vital shield. Shockingly, the average cost of a data breach soared to $4.35 million in 2022. Many assume this protection is just about writing a check when disaster strikes, but cyber insurance does much more. It pushes companies to strengthen their own defenses and rethink their entire approach to digital risk.

Cyber Insurance Guide: Overview and Key Sections

- Defining Cyber Insurance And Its Purpose

- The Importance Of Cyber Insurance In Today’s Digital Landscape

- How Cyber Insurance Policies Work And What They Cover

- Key Concepts And Terms In Cyber Insurance Explained

- Real-World Examples Of Cyber Insurance In Action

Quick Summary

| Takeaway | Explanation |

|---|---|

| Cyber insurance is essential for modern businesses. | As organizations face increasing digital threats, cyber insurance helps safeguard financial stability and operational integrity. |

| Policies provide both first-party and third-party coverage. | These distinctions ensure protection for internal losses and liabilities to external parties, enhancing overall risk management. |

| Proactive cybersecurity practices are crucial. | Cyber insurance complements existing defenses and requires organizations to implement comprehensive security measures for coverage. |

| Risk assessments determine policy premiums and coverage. | Insurance providers evaluate vulnerabilities to tailor coverage, necessitating organizations to maintain robust cybersecurity frameworks. |

| Successful implementation requires ongoing vigilance. | Organizations must continually adapt their defenses and incident response strategies alongside their cyber insurance for effective risk management. |

Defining Cyber Insurance and Its Purpose

Cyber insurance represents a specialized form of risk management designed to help organizations mitigate potential financial losses resulting from digital security incidents. As businesses increasingly rely on digital infrastructure, understanding cyber insurance becomes critical for protecting valuable assets and maintaining operational continuity.

What Exactly is Cyber Insurance?

Cyber insurance is a comprehensive risk transfer mechanism that provides financial protection against various digital threats and potential cybersecurity breaches. Unlike traditional insurance policies, cyber insurance specifically addresses the unique risks associated with digital operations, data management, and technological vulnerabilities.

Key characteristics of cyber insurance include:

- Coverage for direct financial losses from cyber incidents

- Protection against potential legal and regulatory expenses

- Support for business interruption and recovery costs

- Assistance with data breach response and customer notification

The Core Purpose of Cyber Insurance Protection

The fundamental purpose of cyber insurance extends beyond simple financial reimbursement. According to Travelers Insurance, cyber insurance serves as a strategic risk management tool that helps organizations respond effectively to digital security challenges.

Businesses invest in cyber insurance to:

- Minimize potential financial devastation from cyber attacks

- Provide structured response protocols during security incidents

- Demonstrate proactive risk management to stakeholders and clients

- Access expert resources for incident investigation and recovery

How Cyber Insurance Works in Practice

When a covered cyber incident occurs, the insurance policy typically activates a comprehensive support mechanism. This includes financial compensation for direct losses, technical support for incident response, legal assistance for potential regulatory investigations, and resources to help restore systems and reputation.

Key Insight: Cyber insurance is not a replacement for robust cybersecurity practices but a complementary risk management strategy that provides an additional layer of protection and financial resilience.

The Importance of Cyber Insurance in Today’s Digital Landscape

The digital transformation of businesses has dramatically increased cybersecurity risks, making cyber insurance no longer a luxury but a critical necessity. Organizations across all sectors now face unprecedented threats that can potentially compromise their entire operational infrastructure and financial stability.

The Rising Threat Landscape

Cybercrime has evolved into a sophisticated global industry, with attacks becoming more frequent and complex. According to IBM’s Cost of Data Breach Report, the average total cost of a data breach reached $4.35 million in 2022, underscoring the significant financial impact of digital security incidents.

Key emerging cybersecurity challenges include:

- Ransomware attacks targeting critical infrastructure

- Sophisticated phishing schemes

- Supply chain vulnerability exploitation

- Advanced persistent threats from state-sponsored actors

Financial and Operational Protection Mechanisms

Cyber insurance serves as a critical financial shield for organizations, providing comprehensive protection beyond traditional risk management strategies. The coverage extends well beyond immediate monetary losses, encompassing broader operational recovery and reputation management.

Businesses benefit from cyber insurance through:

- Immediate financial compensation for direct losses

- Comprehensive incident response support

- Legal and regulatory compliance assistance

- Professional forensic investigation resources

Strategic Risk Management Approach

Proactive defense is now the cornerstone of modern cybersecurity strategy. Cyber insurance represents more than a financial safety net – it is a strategic tool that compels organizations to develop robust security frameworks and incident response protocols.

By requiring thorough risk assessments and implementing stringent security standards, cyber insurance providers incentivize businesses to continuously improve their digital resilience. This approach transforms insurance from a passive financial instrument into an active risk management partnership that drives organizational cybersecurity maturity.

How Cyber Insurance Policies Work and What They Cover

Cyber insurance policies represent complex risk management instruments designed to protect organizations from the financial and operational consequences of digital security incidents. Unlike traditional insurance products, these specialized policies offer comprehensive protection tailored to the unique challenges of modern technological environments.

Policy Structure and Coverage Components

Cyber insurance policies typically encompass multiple layers of protection, addressing various potential digital risks. According to Congressional Research Service, most policies operate on either claims-made or occurrence basis, providing financial safeguards across different scenarios.

Key coverage components generally include:

- Direct financial losses from cyber incidents

- Incident response and forensic investigation expenses

- Legal and regulatory compliance costs

- Business interruption compensation

- Reputation management and public relations support

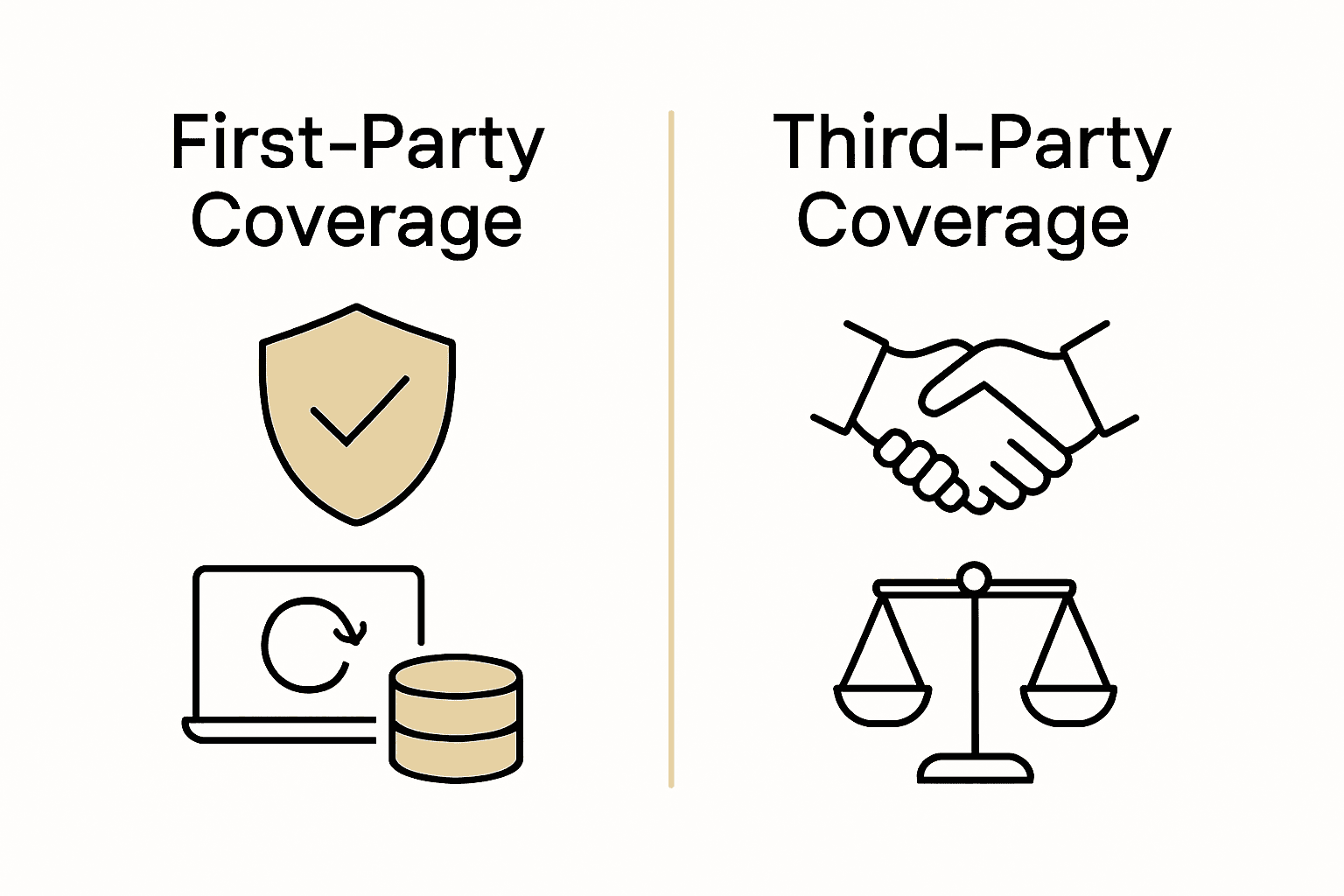

First-Party and Third-Party Protections

Cyber insurance distinguishes between first-party and third-party coverage, addressing different types of potential digital risks.

First-party coverage protects an organization’s own losses and immediate expenses, while third-party coverage addresses potential legal claims and external stakeholder impacts.

First-party coverage protects an organization’s own losses and immediate expenses, while third-party coverage addresses potential legal claims and external stakeholder impacts.

Below is a comparison table outlining the differences between first-party and third-party cyber insurance coverage to clarify their distinct roles within a policy:

| Coverage Type | What It Protects | Typical Costs Covered |

|---|---|---|

| First-Party | Your organization’s direct losses from a cyber incident | Data restoration, lost income, extortion expenses, customer notification |

| Third-Party | Legal claims and liabilities involving external parties | Legal fees, regulatory fines, costs of lawsuits |

First-party protections typically cover:

- Data restoration costs

- Cyber extortion expenses

- Lost income during system downtime

- Customer notification and credit monitoring services

Risk Assessment and Policy Customization

Insurance providers conduct thorough risk assessments to determine appropriate coverage levels and premiums. This process involves evaluating an organization’s existing cybersecurity infrastructure, technological vulnerabilities, and potential exposure to digital threats.

Important Consideration: Cyber insurance is not a substitute for robust cybersecurity practices. Insurers often require organizations to demonstrate comprehensive security measures and ongoing risk management strategies as a prerequisite for coverage. The most effective approach combines proactive security protocols with strategic financial protection.

Key Concepts and Terms in Cyber Insurance Explained

Navigating the complex world of cyber insurance requires understanding specific terminology and technical definitions that shape policy structures and coverage mechanisms. Organizations must develop a clear comprehension of these specialized terms to effectively select and leverage cyber insurance protection.

The following table summarizes essential cyber insurance terms and definitions to help you navigate common policy language:

| Term | Definition |

|---|---|

| Covered Events | Specific digital incidents eligible for insurance compensation |

| Deductibles | Amount paid by the insured before insurance coverage activates |

| Exclusions | Scenarios or incidents not protected under the policy |

| Aggregate Limits | Maximum total insurance payout for all claims during the policy period |

| Per Occurrence Limits | Maximum amount payable for a single covered incident |

| Sublimits | Caps for certain types of covered incidents within the main limit |

| Extended Reporting | Additional time to report incidents after policy expiration |

Essential Policy Terminology

Cyber insurance policies incorporate precise legal and technical language designed to define coverage boundaries and operational parameters. According to National Conference of State Legislatures, policy terms frequently establish critical definitions that determine the scope of financial protection.

Key foundational terms include:

- Covered Events: Specific digital incidents eligible for insurance compensation

- Deductibles: Predetermined financial amounts an organization must pay before insurance coverage activates

- Exclusions: Particular scenarios or types of cyber incidents not protected under the policy

Technical Risk Assessment Definitions

Insurance providers utilize specialized terminology to evaluate and categorize organizational digital risk profiles. Risk scoring represents a comprehensive method of quantifying potential cybersecurity vulnerabilities and determining appropriate coverage levels.

Critical risk assessment concepts encompass:

- Threat vectors

- Vulnerability assessment

- Potential financial impact

- Likelihood of occurrence

- Historical incident data

Policy Structure and Limit Terminology

Cyber insurance policies employ specific terms to define financial protection frameworks. Understanding these terms enables organizations to make informed decisions about their digital risk management strategies.

Important policy limit concepts include:

- Aggregate limits

- Per occurrence limits

- Sublimits for specific incident types

- Extended reporting periods

Critical Insight: Precise comprehension of cyber insurance terminology transforms these policies from complex legal documents into strategic risk management tools. Organizations must carefully analyze each term to ensure comprehensive protection aligned with their specific technological infrastructure and potential digital vulnerabilities.

Real-World Examples of Cyber Insurance in Action

Cyber insurance has transitioned from a theoretical risk management concept to a practical protective mechanism for organizations facing increasingly sophisticated digital threats. Real-world scenarios demonstrate how these policies provide critical financial and operational support during complex cybersecurity incidents.

Healthcare Sector Incident Response

Healthcare organizations, managing sensitive patient data and complex technological infrastructures, represent a prime example of cyber insurance’s practical application. A significant data breach can potentially compromise millions of patient records and result in substantial financial and reputational damage.

Typical healthcare cyber insurance scenarios include:

- Covering forensic investigation costs after a ransomware attack

- Supporting legal expenses related to regulatory compliance violations

- Providing funds for patient notification and credit monitoring services

- Compensating for lost revenue during system restoration

Manufacturing Supply Chain Protection

Manufacturing companies increasingly rely on interconnected digital systems, making them vulnerable to sophisticated cyber attacks that can disrupt entire production networks. According to the U.S. Government Accountability Office, cyber insurance helps organizations manage the complex aftermath of digital security incidents.

Key manufacturing cyber insurance applications include:

- Addressing business interruption caused by system compromises

- Covering costs of technological infrastructure restoration

- Supporting incident response and threat mitigation efforts

- Protecting against potential intellectual property theft

Financial Services Risk Mitigation

Financial institutions face unique cybersecurity challenges due to the sensitive nature of their digital transactions and customer information. Cyber insurance provides a critical safety net for managing potential financial and reputational risks associated with digital security breaches.

Critical Insight: These real-world examples illustrate that cyber insurance is not merely a financial instrument but a comprehensive risk management strategy. Successful implementation requires organizations to develop proactive cybersecurity practices alongside robust insurance coverage, creating a multi-layered approach to digital risk protection.

Protect Your Business Beyond Insurance—Build Real Cyber Resilience With SRS Networks

Reading about cyber insurance highlights just how complex and relentless cyber threats have become. While a good cyber insurance policy can help you recover financially after a digital attack, the real pain point is preventing these crises in the first place. Managing covered events, staying compliant, interpreting policy exclusions, and keeping your business reputation intact are huge concerns that insurance alone cannot fully solve. You need practical defenses and a partner you can trust.

Do not wait until you are facing a devastating breach or regulatory fine to discover gaps in your security. Take control now by partnering with SRS Networks, your local cybersecurity and IT specialist. We deliver hands-on support, proactive monitoring, and tailored cybersecurity solutions that help you meet compliance, prevent downtime, and boost confidence for clients and stakeholders. Ready to combine strong protection with trusted local support? Contact SRS Networks today and turn your cyber insurance strategy into a true shield for your business future.

Frequently Asked Questions

What is cyber insurance?

Cyber insurance is a specialized form of risk management that provides financial protection against various digital threats and cybersecurity breaches. To understand its benefits, evaluate how your organization relies on digital infrastructure and consider obtaining a policy tailored to those specific risks.

How does a cyber insurance policy work in practice?

When a covered cyber incident occurs, the policy activates a support mechanism offering financial compensation for direct losses, incident response assistance, and legal help. Start by reviewing your policy details to ensure you know the coverage limits and the steps required for filing a claim after an incident.

What types of incidents are typically covered by cyber insurance?

Cyber insurance policies usually cover direct financial losses from cyber incidents, incident response costs, regulatory compliance expenses, and business interruption support. Examine your organization’s vulnerabilities to identify which specific types of incidents to discuss with your insurance provider.

How do I assess the level of coverage I need for my business?

Assessing your coverage needs involves evaluating your current cybersecurity practices, potential financial impacts of incidents, and historical data on cyber threats relevant to your industry. Conduct a thorough risk assessment and consult a professional to determine appropriate coverage levels for your organization.

Are there prerequisites for obtaining cyber insurance coverage?

Insurance providers often require organizations to demonstrate robust cybersecurity measures and ongoing risk management strategies before approving coverage. Begin by implementing comprehensive security protocols and documenting your risk management efforts to enhance your eligibility for a policy.

What is the difference between first-party and third-party cyber insurance coverage?

First-party coverage protects your own organization’s losses resulting from a cyber incident, while third-party coverage addresses legal claims and impacts affecting external stakeholders. Review your business operations to identify which coverage type is more critical for your risk management strategy.